The Artisanal Spirits Company’s flagship brand is The Scotch Malt Whisky Society, which curates unique ultra-premium single cask Scotch malt whiskies and other spirits.

Sales are made exclusively to its subscription-paying members, of which there are just over 29,400 according to the latest update. Members pay an annual subscription currently priced at £65.

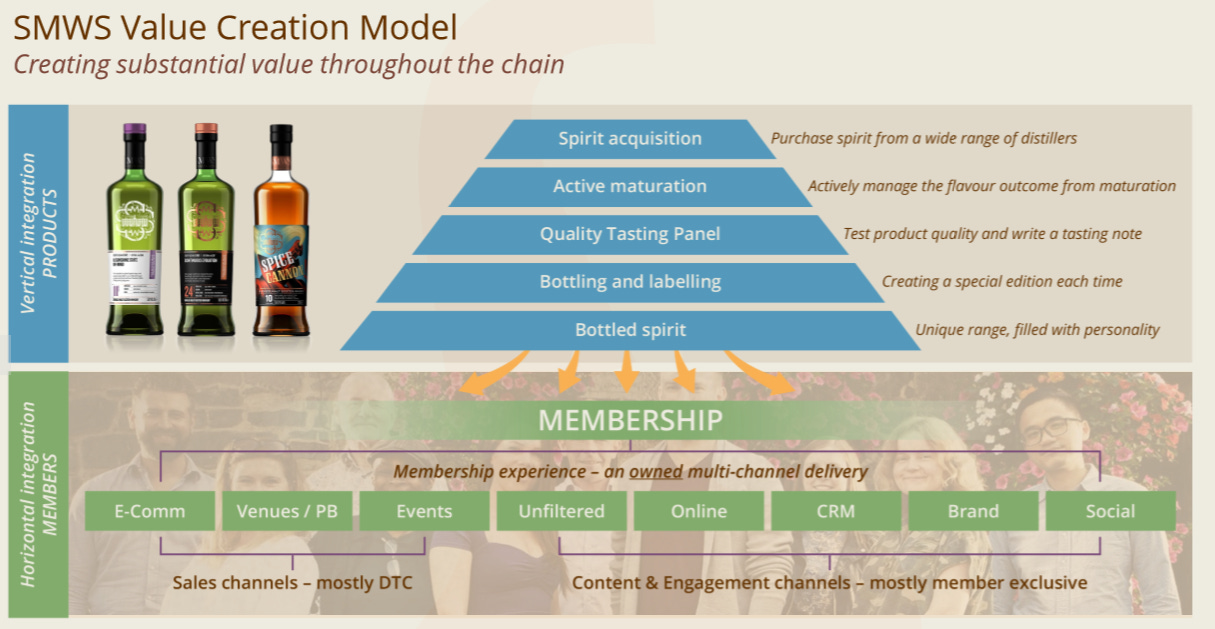

TSMWS selects casks from over 100 primary producers. They then actively manage the maturation process, which is the key stage to developing multiple flavours. Once the process is complete, the finished product is sold directly to members. Its product prices typically range from £45 to over £1,500 per bottle.

Only 250 bottles of each new edition is sold, making this rare, exclusive, and highly desirable for members.

Currently 90% of sales are made direct to consumer (D2C), via its own website. Remaining sales also come via partner bars situated around the world.

In 2017 the Company acquired the legal rights to the J.G. Thomson & Co. brand with the vision of reviving its renowned blended whisky heritage.

The relaunch the J.G. Thomson & Co. brand should happen this year. Bottles are already being pre-sold via the website. This brand will also be sold via supermarkets, clubs, bars, and other retail outlets.

Brief History

The Scottish Malt Whiskey Society was started in 1983 by malt whisky enthusiast Philip “Pip” Hills.

Mr Hills who had experience of forming syndicates, started to purchase single casks of malt whisky for maturation and bottling.

He later made the decision to broaden the process by forming a membership group, which had its first premises in the Vaults in Leith, Edinburgh.

If you’re interested in learning more about the history of the club I would suggest reading Mr Hill’s book called The Founder's Tale: A Good Idea and a Glass of Malt which details the early days of his venture.

In 2005 The SMWS was acquired by malt whisky distiller Glenmorangie, which was itself taken over by international luxury goods and drinks company LVMH in the same year.

It became apparent that SMWS was not going to be part of their future plans. Even if LVMH doubled the size of SMWS it would still be small fry for a company of their size. So in 2014, LVMH sold the company to a group of private investors.

In 2018 further investment was made into the business by Inverleith, a locally based private equity investor, which proved transformational.

The new investment enabled the SMWS to double revenues, quadruple the scale of its stock of casks, and grow the proportion of sales to overseas’ members from under 25% to nearly 70%

SMWS returned to public ownership with the flotation of Artisanal Spirits in 2021 on London’s AIM exchange.

Business Model

The business model is a direct-to-customer subscription service.

Each member pays £65 per year to be in the club. This recurring revenue forms the building block of revenue. On top of this comes this actual sales of whisky to the members.

The cost to acquire a new customer in the UK is £65, so they get the marketing spend back on day 1.

Each member stays for an average of 4 years and contributes £276 in membership fees. The Life Time Value LTV of each member with fees and bottle purchases added together is £932.

Big margins on each bottle

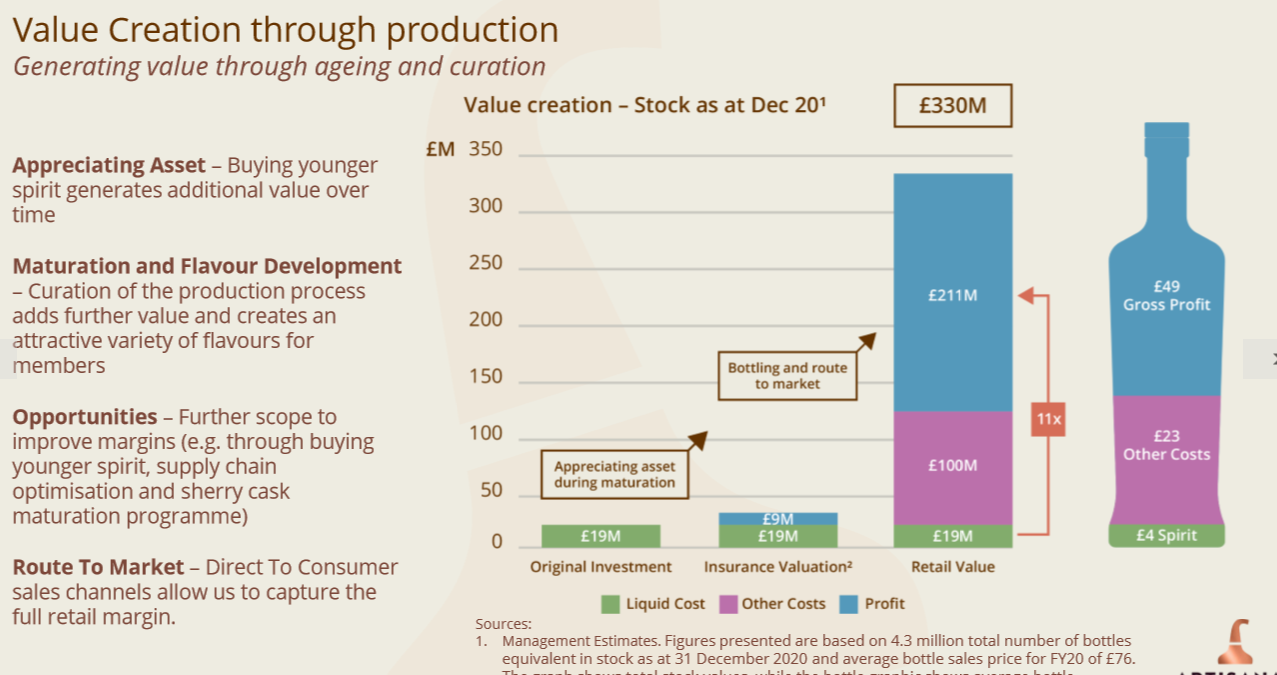

According to the company each cask appreciates in value at about 10% per annum as the young whisky ages.

For every £1 spent on acquiring liquid stock the company generates £11 of gross profit. These profit margins will increase further as the company focuses on buying younger spirit, and supply chain optimisation.

What do they do differently?

As you can imagine there is a great deal of competition in the premium spirits space.

However, there are things that Artisanal do differently. I’m not sure I would call these things a moat, but they do lots of small things differently which when added together makes them stands out from competitors.

Such as…

Ltd edition bottles

Creating unique tasting whisky

Original producer protection

Brands

Pricing power

Loyal customers

Lower costs

Let’s look at some of these attributes individually…

Limited Edition

The company only produces around 250 bottles of each new whiskey. This makes each bottle unique, exclusive, and rare. I haven’t found many other Scotch whiskey brands that limit the supply of each whisky.

This strategy generates demand, as whisky lovers feel a fear of missing out running through their veins.

Many people also buy whisky as an investment.

If you are seeking to add exposure to whisky in your portfolio then buying shares in this company could be a great way to do it.

As central banks keep expanding their currencies faster than the universe, we may see whisky investing grow in popularity, which will act as a tailwind for the company.

Producer Protection

Another key differentiator is the SMWS policy of not revealing the distillery’s name on the label. This policy encourages the consumer to exclusively focus on the unique flavor of each batch.

Importantly, by protecting the identity of the original producer, SMWS products do not compete for brand recognition with its partner distillers.

Brands

While it’s much easier these days for any old Jim and Jane to create their own drinks brand - to create a subscription model over a 40 year period, to have connections with the best distillers, and (eventually) your own warehouse, would take some doing. All these attributes makes ART more secure and profitable than other smaller artisan brands.

The main competition comes from the big boys in the industry such as Brown-Forman. However, ART distance themselves from these guys by being limited, vintage, and selling direct to their customer. There is enough room for them to survive and prosper in this huge global industry.

Total Addressable Market

According to the company the premium segment of the whisky market they’re targeting is worth about $4.2 billion, and between 2010-19 grew at a CAGR of 10%.

This is a secular growth trend driven by higher earning power, especially in Asia. Despite the pandemic, this trend should continue over the rest of this decade.

Most of this growth has come from the 8 markets featured in the table below.

Currently the company has captured just 0.4% of this market.

Lets no forget about India. This is a burgeoning market for whisky drinkers. ART has barely touched the service in this country.

Opportunity For Growth

There is plenty of opportunity to increase revenue.

The company has formulated the following growth strategy to do just that. >

Generating more sales with existing members

Converting more people to become members via their ecommerce shop, and through their hosted nights at physical venues.

International Expansion

Having initially proven its premium experience model in the UK, SMWS is now expanding to international markets, with 69% of 2020 sales from outside the UK. They now have members in 30 different countries.

43% of the growth of the last two years came from the key markets of the US and China.

They have recently launched an EU site, and a Japanese ecommerce store is planned.

A key focus on improving margins

Buying younger spirit which costs less, but once mature sell for higher prices.

At the moment the company outsources the storage of the whisky to third parties. They are now in the process of building a modern storage facility to house their own stock.

This upfront cost is estimated to be £2.2m. However, once built this will improve the overall margins as there will be no more third party costs to bare.

Creating new brands outside of SMWC

As previously mentioned they are due to launch the JG Thomson brand. They are also looking into building an American Malt Whiskey Society, as well as exploring opportunities in other spirits such as rum and gin.

Financials

Since SMWC was bought from LVMH the revenue growth has been impressive.

Between FY16 and FY19, revenues almost doubled from £7.6 million to £14.6 million, representing a CAGR of 24%.

Judging from the companies most recent update it looks like that kind of growth rate is starting to reappear now venues are back open.

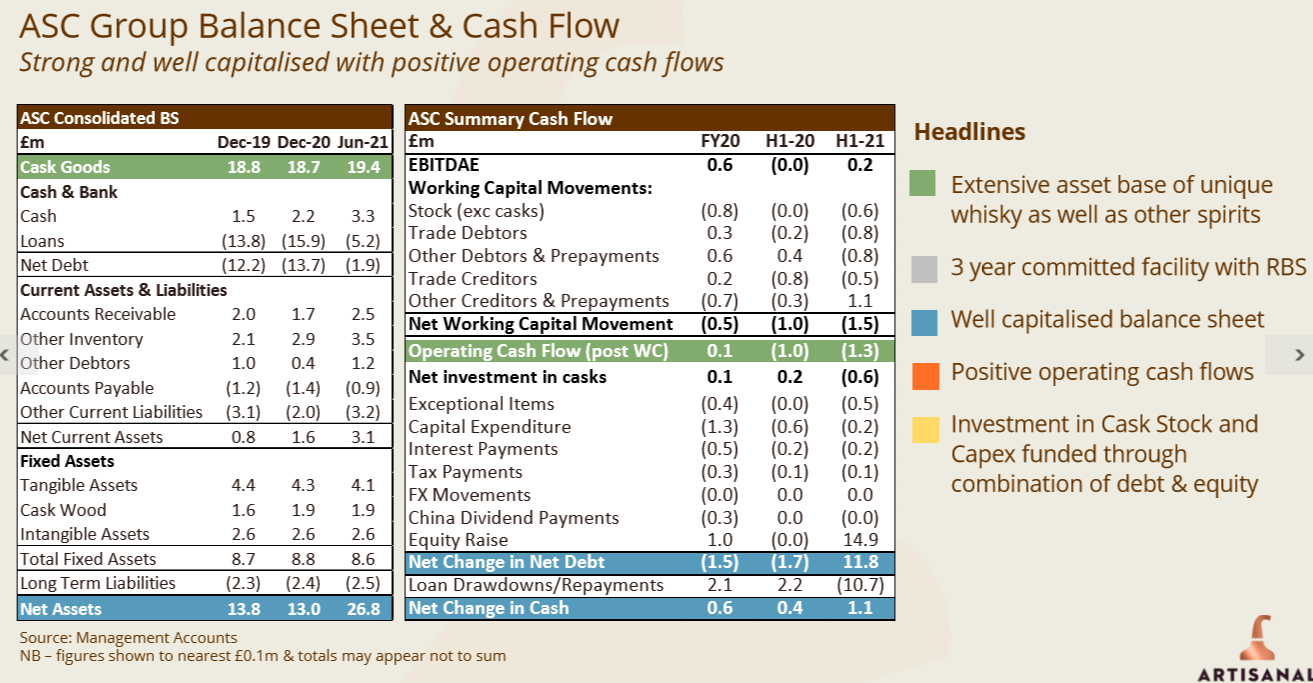

The balance sheet is healthy with manageable debt. It is worth noting there are hard assets on the balance sheet in the form of whisky stock, casks etc. The stock of whisky is worth £220m in gross profit. These assets do not show on the balance sheet.

This is the case with many companies especially drinks companies, however to have that level of stock above the current market cap should be noted.

Management

The management team is experienced, and has a great blend (excuse the pun) of people who have worked previously for alcohol companies, luxury brands, accounting firms, and in capital markets.

Look how smart they look in front of all those whiskey bottles.

(source: artisanal-spirits.com)

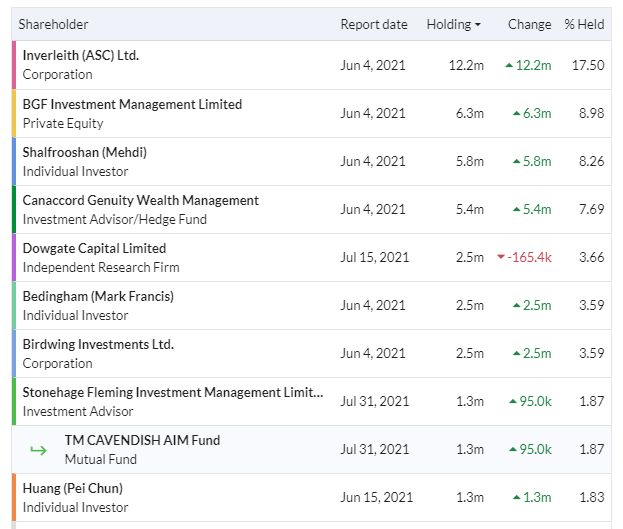

The current shareholder line-up stands as follows…

Note there has only been one shareholder selling since the IPO, and even then it’s not been much. Interestingly enough that seller was Dowgate Capital who own Dowgate Wealth.

Jeremy recently published a blog on the Dowgate website about why he likes Artisanal Spirits, which I reference at the end of this article. So I’m not too concerned with their recent sale of shares.

Directors Buying

As you read more Capital Employed Letters you will notice we are big fans of founders, families, management, and employees with skin in the game.

Unfortunately there is not a huge amount of insider ownership.

Mark Hunter, the CEO, owns 1.36%, and Ned Bedingham, the Non-Executive Director, owns 3.59%.

There has also been recent director purchases on the 16th September after the results were published. This is an encouraging sign.

Valuation

Putting together this report has been fairly easy as the company does a great job of providing investors with all the information.

Placing a valuation on the company and working out if it’s undervalued at current market cap is not so easy.

At an operating level ART is loss making, however this is by choice, as they keep reinvesting in future growth.

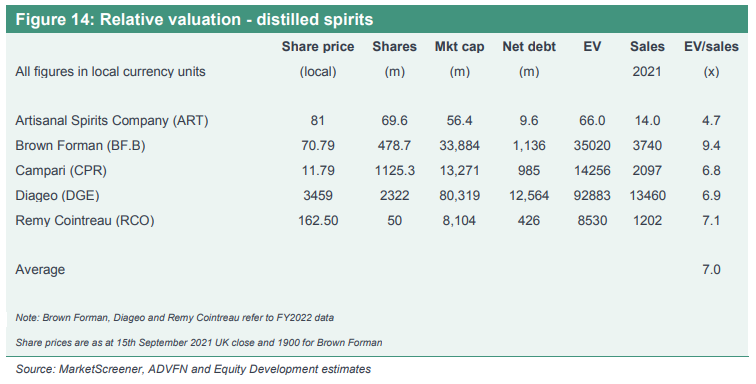

Equity Development, a research house in London, has valued ART using a comparative approach. The report states…

‘Given the company’s relatively early stage as a listed company and its current high gross margin pre-EBITDA status, we argue that EV/sales ratio is the most appropriate first stage comparison.

For Artisanal Spirits Company’s shares (LON:ART) to trade in line with this peer group the stock price would have to rise to 150p.’

The research report also adds…

‘…we note that were Artisanal Spirits Company’s shares to trade at our 150p fair value they would have an EV/gross profit multiple less than one point above group average.

However, given that significant gross profit margin growth is a clear management expectation, as discussed in this report, and that ASC reports its sales gross of duty such a premium would be justifiable in our view.’

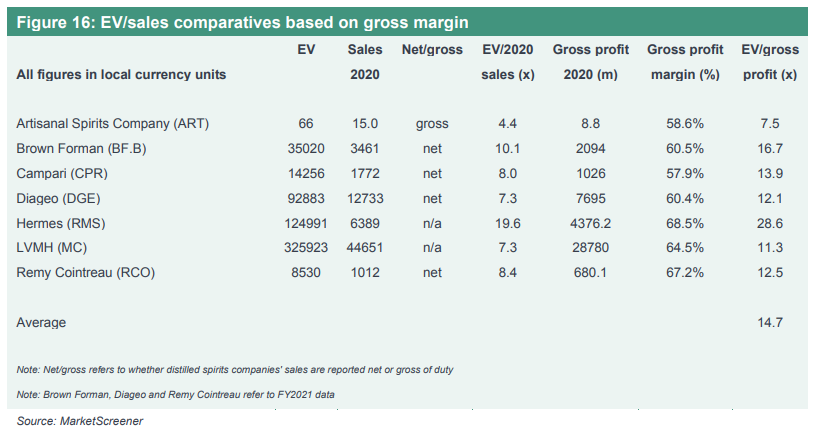

Let’s not forget all the whisky it has in stock on the balance sheet in the form of its cask and bottled inventory.

This inventory stands at a book cost of £21m and represents over 15,000 casks of spirit (each a specific new product). There is enough stock to last until 2026.

The realisable gross profit from its whisky stocks is estimated to be £220m, that’s a 70% discount from the current market cap.

Back of the Whisky Mat Calculations

The following calculation is very crude way of determining a valuation but one worth thinking about.

If you look at similar competitors who are publicly listed they all have excellent operating margins.

Brown-Forman 36%

Campari 18.8%

Diageo 28%

Remy Cointreau 20%

Pernod Ricard 21.9%

(source: Stockopedia.com)

The average operating margin of the above 5 companies is just shy of 25%.

ART are predicting revenue of £22m for 2022. If they were to eventually (one day in the future, not now) start converting 25% of the revenue into operating profit with current figures that would equate to £5.5m.

I think a conservative PE in today’s markets for a company growing sales at the pace of ART would be about 20.

Quick math’s…

20 x 5.5m = £110m market cap.

That’s 44% above todays market cap, and would give a price per share (if they don’t add more shares) equal to 159p. That is not far away from Equity Developments target of 150p based on their relative valuation method.

Of course £22m is just a standstill number, over the years the revenue will grow higher than that, which makes the current share price look reasonable in my view.

Risks

The following risks for are worth thinking about…

Poor marketing

Another company we own in the Capital Employed Portfolio is Naked Wines, who do an outstanding job of promoting to, and conversion of, new members.

It seems Artisanal are not as aggressive in customer acquisition. However, this shouldn’t be seen in a negative light.

Every company does things differently in this regard, but the marketing strategy is something to keep a close eye on.

They had an excellent opportunity to do more online marketing during the pandemic to help build their direct-to-customer online sales. Unfortunately the sales during the covid period of 2020 more or less remained flat.

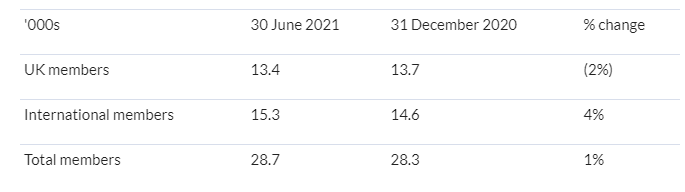

If we also look at the latest company update for the half year results released on 16th September 2021, the membership declined in the UK by -2%, however international members grew by 4%, meaning the total growth in members was just 1%.

For the online marketing strategy management mention live tasting on their YouTube channel, but don’t reveal more than that.

However, lets be fair they don’t want to let competitors know what their strategy is. So I will give them the benefit of doubt regarding this.

They have recently hired a marketing/ecommerce director. Recruitment of new members has to be much higher if they are to hit their target of 40,000 members.

Management said that the beginning of H2 has been very positive.

Still making a loss

Despite rapid growth in the number of members and revenue, ART generates operating losses at the group level; however, this is mainly a function of investment in growing its global membership, launching a new retail brand, and building there own warehouse to store the whiskey. The profits should appear in the not too distance future.

Regulation

ART is vulnerable to changes in regulation, duties and tariffs that may affect customer demand and ASC’s profitability.

Spirit Problems

No I don’t mean problems with ghosts I mean problems that could happen to the maturing spirits in storage. If this stock got damaged the company would take a hit to growth. Yes they would get the insurance payment but it would take time to build that type of inventory again.

Conclusion

The investment case is simple. The company has award winning products, heritage brands, huge margins, and has a great opportunity to grow into the expanding worldwide premium spirits trend.

The management and employees are experienced and seem to have a real passion for what they do.

I am excited to see what they can achieve with the brand they are launching outside of the SMWS. This should help grow, and diversify, revenue streams.

Whisky and spirits have been drunk for hundreds for years and will be for hundreds of years to come. Added to that the inflation protection that whisky offers, and we’re bullish on the company.

Their aim is to double sales by 2024, lets see if they can do it.

The writer holds shares in the Artisanal Spirits Company. The company also features in the Capital Employed Portfolio.

The above article is for informational and educational purposes only, and should not be seen as investment advice. Please do your own research before thinking of investing in any company mentioned.

Nice write up! Looking worward to more write ups, not that much of a podcast fan in general...

could you elaborate on the valuable assets not accounted for on the balance sheet ?

Best, s4v