This Dutch Microcap is Plastic Fantastic

This Dutch Microcap is Plastic Fantastic

Sometimes it’s the boring, under followed companies quietly going about their business that can make great long-term investments.

Capital Employed Letter #1

Reading time: 7 minutes

Holland Colours NV is a quality, well-managed company with high returns on capital.

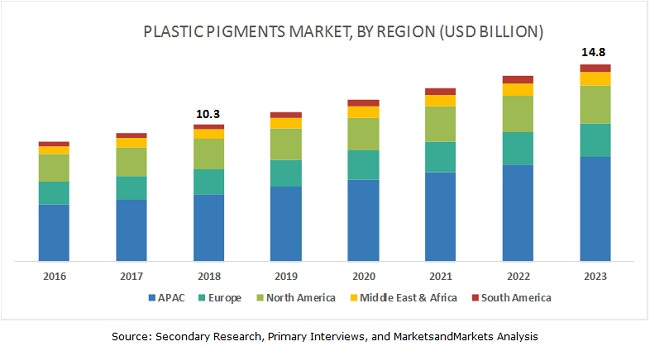

The company operates in an industry that is often ignored and growing just shy of 8% per year.

Sometimes it’s the boring, under followed companies quietly going about their business that can make great long-term investments.

Table of Contents:

Key Facts

What does the company do

Who are its customers

Its products

Management

Growth Opportunity

Competition

Financials

Valuation

Risks

Conclusion

Key Facts

Company name: Holland Colours NV

Ticker: HOLCO

Listed: Euronext Amsterdam Stock Market

Market Cap: 151m euros

Incorporated: 1979

Public since: 1991

Website: hollandcolours.com

What does the company do?

Holland Colours NV is a manufacturer and supplier of pigments, granulates and pastes.

To put it more simply… all plastics (resin) are nearly colorless or milky-white.

The company manufactures the pigments which are added to produce plastic products in various colors.

Who are the customers it supplies?

In 2020 the company colored over 2 billion kilograms of plastic.

It has a broad and diversified set of customers, with over 2,000 customers in 85 countries.

The Company is organized in three regional divisions:

Europe (including the Middle East, India and Africa)

The Americas

Asia

It has production sites in the Netherlands, Hungary, United States, and Indonesia.

The company focusses efforts on three markets:

Building & Construction –>

Comprising of colorants for pipes, fittings, cladding, siding, window profiles, roofing materials and fences;

Plastic Packaging –>

Including color preparations for PET packaging of food and drink, cosmetics and personal care products.

Silicones & Elastomers –>

Including colorants for sealants and silicone rubber products.

Products and Process

So how does plastic get its colour?

The most common method used by molders, masterbatches consist of concentrated pigments dispersed into a polymer carrier resin.

During molding the masterbatch is let down into natural resin as it is feed into the press at a predefined ratio to achieve the desired color.

Holland Colours produces concentrates for coloring plastics.

These are available in both solid and liquid form and applicable for various types of plastic materials, particularly for polyvinyl chloride (PVC) and polyethylene terephthalate (PET).

They have been pioneering eco-friendly coloring for many decades now. Their products are IP supported.

They keep innovating and investing in further research and development of new products.

The company has long recognised the move into more eco-friendly plastics.

Below is an extract taken from the latest annual report…

‘We continue to work on new applications for our sustainable carrier technology.

In addition to our bio-based color concentrates, we now use the same technology to make additive concentrates, including some specifically designed to support packaging, product or process sustainability, and to enhance bottle recycling.

Low dosing, enhanced recyclability and reductions in scrap rate and energy consumption are the key drivers.’

TasteGuard, for example, helps to ensure that bottled water tastes of water, not the container they come in.

LightGuard extends the shelf life of teas and juices by protecting them against UV.

TintMask counteracts the yellow appearance of recycled PET bottles, boosting their acceptance among consumers.

FastHeat reduces the energy needed to produce PET bottles.

Holcomer Thermostretch complies with new EU regulations to limit the use of titanium dioxide, while reducing the energy consumption during the bottle blowing process.

Management and Employees with Skin in the Game

The majority shareholder is Holland Pigments BV, who owns 50%.

Holland Pigments BV was founded in 1980 and owns the majority of the shares of the listed company Holland Colours NV since April 2, 2012.

All the employees worldwide have an interest in Holland Colours via shares in Holland Pigments BV.

Other key shareholders include Gert Hein de Heer, whose father founder Holland Colours.

It is great to see the de Heer family still involved, and employees have a big stake in the business.

The Opportunity in a Plastic Nutshell

So now we have added a bit of colour to the background of the company (I know, stupid pun) lets look more into the opportunity.

Now just take a moment to look around you, I bet you there are plastics everywhere right? And all that plastic has been coloured.

Just to put that in perspective, the average worldwide growth of ecommerce is 11%.

The high demand for packaging in emerging countries is leading to the increasing consumption of plastic pigments.

The growing packaging industry along with rapid industrialisation in the region is a key factor driving the plastic pigments market in all regions.

Plastic goods are also replacing heavy metal products in various applications due to their cost efficiency and lower weight.

China is the largest market of plastic pigments in the region, in terms of volume, due to the high demand of plastic pigments in the plastics industry.

However, APAC is projected to register the highest growth in the global plastic pigments market during the forecast period.

The demand for plastic pigments is projected to increase in India due to the economic development and the strong presence of small players in the plastic pigments market.

Competition

It would be very difficult to start a company from scratch to manufacture plastic pigments.

Unless you have guaranteed customers lined-up, why would you bother investing in plants, machines, employees etc. it would be too risky.

Of course I could be wrong, we may see the rise of competitors from India for example, however I think the main competition is from existing players.

Other companies around the world who manufacture pigments include…

Clariant (Switzerland)

BASF (Germany)

DIC (Japan)

Huntsman (US)

Cabot (US)

LANXESS (Germany)

Chemours (US)

Heubach (Germany)

Tronox (US)

Ferro (US)

All of these companies are much bigger than Holland Colours, and do other things besides plastic pigment colouring such as specialty chemicals.

All the companies listed above have large debts, big pension liabilities, and sluggish growth.

Holland Colours is the complete opposite - it’s smaller, more nimble, has no debt, or big pension liabilities. Holland Colours is solely focused on becoming the best at plastic pigment colouring.

Interesting side note, Warren Buffet holds a personal 5% stake in Lanxess, so he must see value in having exposure to this basic materials space.

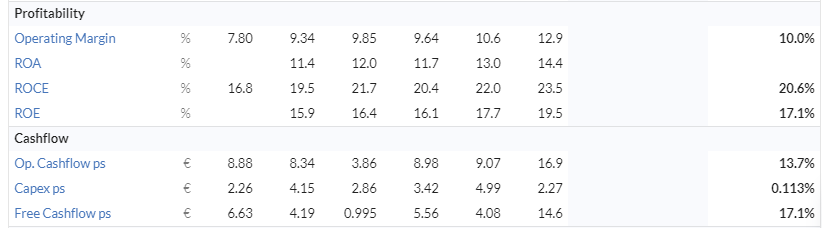

Quality Metrics Shine Through

Holland Colours is far superior on all metrics compared to its rivals.

Operating Margins, Returns, and Free Cash Flow per share are solid:

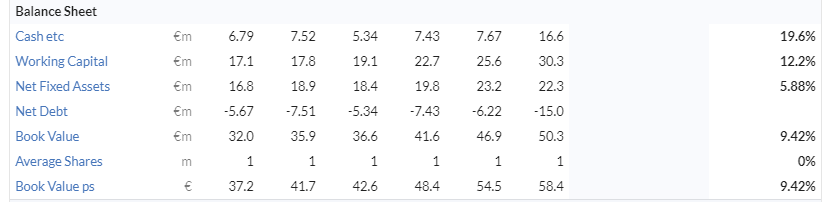

Balance Sheet:

The company has a healthy balance sheet with 16.6 million euros cash in the bank, no debt, with just a small pension liability.

Book value per share has grown every year. And the shares have not been diluted.

It has a Petrotski F-score of 7, which is healthy.

(Please note the above metrics were taken from Stockopedia).

Valuation

Holland Colours is on a higher PE than its peers, however this is to be expected considering it is a higher quality operation.

I bought shares in the company at 87 euros per share in the depths of the covid crash in early 2020. Back then it was on a PE of 8.8. Since then the shares have doubled, the PE is now 15.

Despite the move higher, and higher PE rating, the valuation still looks decent.

EV to EBITA is 8.

Operating cash flow yield of 10%.

So while not an absolute bargain as it was this time last year, it is very reasonable.

The dividend yield is currently 5.37%, which has grown most years, although was paused for 2020 due to covid.

According to the last update published on 3rd June, the revenue for 2020/21 was down by 5%, which considering all the problems caused by lockdowns/covid is not too bad.

However, the net profit and cash flow for 2020/21 was much higher, which shows how well they have managed the covid situation.

Revenue for 2021/22 is predicted to grow by 17% to 113m euros. Lets see if that’s the case.

Risks

The main risks the company could face…

Sourcing material –

The current high demand for raw materials means they face longer delivery times from their suppliers. This is a problem many companies are currently facing.

As the world recovers from the virus and lockdowns these restrictions should start to ease, and hopefully prices come down.

Holland Colours is not dependent on just one key supplier, and operate a dual supplier strategy for key raw materials to mitigate the risk of supply disruption.

Like many companies who have struggled to source materials throughout this covid crisis - in the future they will probably stock higher inventories.

Inflation –

At some point in the future their machines will get older. These will need be replaced, costs for these machines will in all likely-hood be higher.

Changing Trends –

There is always a risk of not keeping up with ongoing changes in market requirements especially regarding plastics, and the subsequent environmental concerns.

If you read the latest annual reports you will see they mention the environment an awful lot of times, and claim to be one of the pioneers of eco-friendly pigments.

Competition -

And of course, competition is a constant risk. Once again, judging by their key financial metrics they seem to be doing a good job at gaining sales, and improving margins - which indicates they are not losing out to their competition.

Conclusion

Holland Colours NV is a well run company, with management and employees who have plenty of skin in the game.

The company has good fundamental momentum in an industry that is expected to grow just shy of 8 % per year.

They are growing faster than many of their rivals previously mentioned in this article.

The net profit has grown by an average of 21% over the past 5 years.

The free cash flow per share has grown an average of 17% over the past 5 years.

I believe this is one of those boring basic material companies what will keep compounding over the long run.

It is one of those stocks you could (in theory) tuck away for the rest of decade and hopefully do well with both capital appreciation and growth in dividends.

Written by Jon Kingston.

The above article is for informational and educational purposes only, and should not be seen as investment advice. Please do your own research before thinking of investing in any company mentioned.

Full disclosure: The author owns shares in Holland Colours NV.